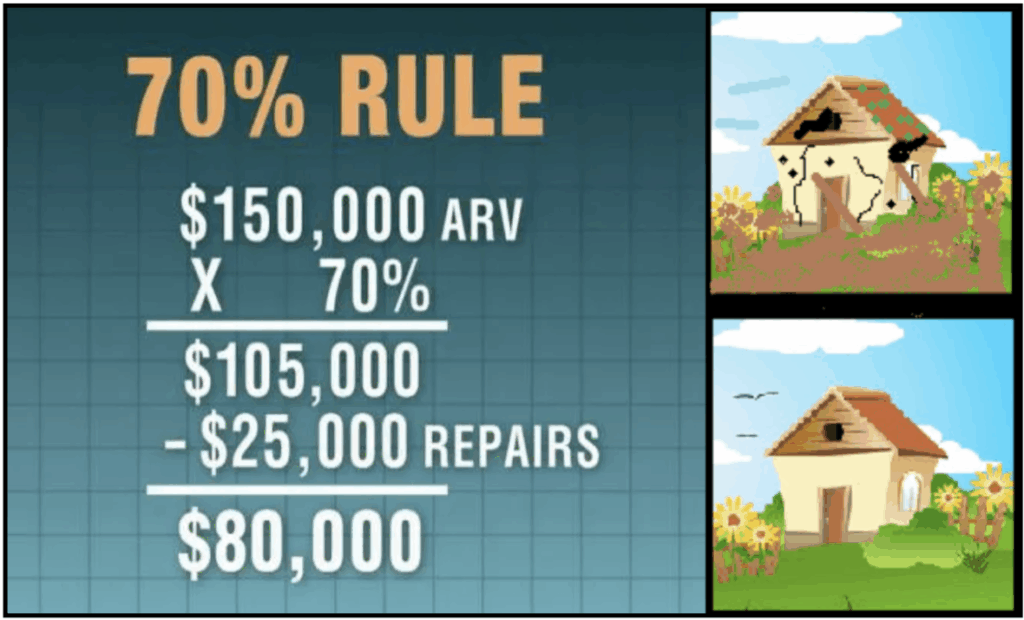

| For a hard money lender like Jump Capital, “fundability” isn’t just about a pretty house; it’s about a math problem that works. In 2026’s more cautious lending environment, lenders are looking for deals that protect their capital while ensuring the investor can exit profitably.Here are the four pillars that make a deal “fundable” from a lender’s perspective. 1. The “70% Rule” and ARV AccuracyThe After Repair Value (ARV) is the North Star of hard money lending. In 2026, lenders are scrutinizing “comps” (comparable sales) more than ever.The Threshold: Most lenders want to see a total loan amount (purchase + rehab) that does not exceed 70% of the ARV.Lender Logic: This 25-30% “equity cushion” protects the lender and you the investor, if the numbers don’t work and you need all your cash to get it closed, is it really a deal?. If your math relies on “record-breaking” neighborhood prices to make sense, the deal is likely unfundable. |

2. A Concrete “Exit Strategy” (Plan A and B)

A lender wants to know exactly how they are getting their money back. A “fundable” deal has a clear, documented path to the finish line.

- Plan A: Usually a retail sale. Lenders look at “Days on Market” for similar homes to ensure you can sell within the loan term (usually 6–12 months).

- Plan B: Can this property “pencil out” as a rental? With higher interest rates in 2026, lenders love to see a DSCR (Debt Service Coverage Ratio) of 1.2 or higher, meaning the rent covers the new mortgage plus 20%.

3. Experience and “Skin in the Game”

While hard money is asset-based, the borrower still matters. Lenders are more likely to fund a deal when the investor has a track record or personal capital involved.

- Liquidity: You must show “proof of funds” for the down payment and at least 3–6 months of interest reserves. A deal where the borrower has $0 in the bank is a massive red flag.

- The “First-Timer” Tax: If it’s your first flip, expect a lower LTC (Loan to Cost). Lenders might only fund 80% of the purchase price instead of 90% until you’ve proven you can manage a budget.

4. Professional Scope of Work (SOW)

A vague “I need $50k for repairs” will get a deal rejected instantly. A fundable deal includes a line-itemized budget.

- The Detail: Lenders look for specific quotes on big-ticket items (HVAC, Roof, Foundation).

- The Draw Schedule: Lenders fund rehab in “draws” after work is inspected. If your SOW doesn’t align with a logical construction timeline, the lender will see it as a management risk.

If some of these items seem out of reach right now, then we want to invite you to Build your network and get the strategies and solutions you need to be successful . To that end, come join us for the I-81 REI meetup this Thursday night, March 26th, starting at 6:30 PM at the Hilton Garden Inn in Martinsburg, WV. It’s a great opportunity to swap strategies, find new deals, and connect with fellow investors who are navigating the same market shifts. Whether you’re a seasoned pro or just getting started with your first flip, we look forward to seeing you there and helping you grow your network.